Are home equity Loans considered taxable income?

By Caleb Butler

Are home equity Loans considered taxable income?

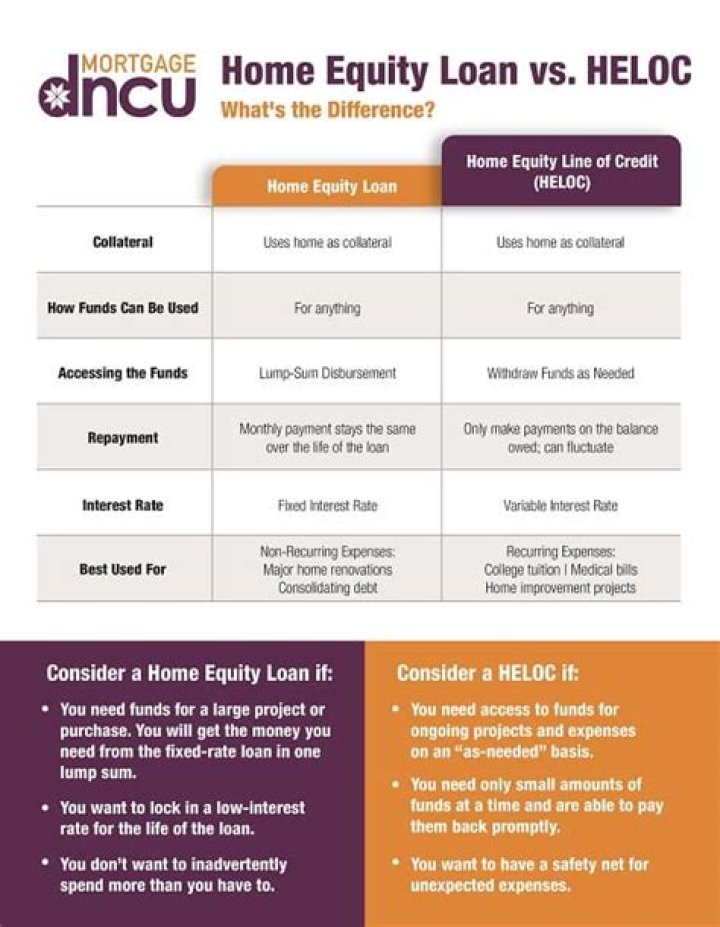

First, the funds you receive through a home equity loan or home equity line of credit (HELOC) are not taxable as income – it’s borrowed money, not an increase your earnings. This may be assessed by your state, county or municipality and are based on the loan amount. So the more you borrow, the higher the tax.

Is a home equity loan tax deductible in 2020?

For 2020, you can deduct the interest paid on home equity proceeds used only to “buy, build or substantially improve a taxpayer’s home that secures the loan,” the IRS says.

How much of a home equity loan is tax deductible?

What Home Equity Loan Interest Is Tax Deductible? All of the interest on your home equity loan is deductible as long as your total mortgage debt is $750,000 (or $1 million) or less, you itemize your deductions, and, according to the IRS, you use the loan to “buy, build or substantially improve” your home.

Do you have to pay tax on equity release?

The short answer is no, there’s no direct tax to pay on the money you receive from an Equity Release plan. When you borrow against your home with a Lifetime Mortgage, it’s not classed as income so there’s no income tax to pay on the money. Equity Release Mortgages are therefore not liable for capital gains tax.

Can I write off home equity loan interest?

Interest on a HELOC or a home equity loan is deductible if you use the funds for renovations to your home—the phrase is “buy, build, or substantially improve.” To be deductible, the money must be spent on the property whose equity is the source of the loan.

Which loans are tax deductible?

Let’s throw light on three important loans that qualify for a tax rebate as per the provisions of the Income Tax Act, 1961.

- Education Loan Repayment: Deductions Under Section 80E.

- Home Loans: Deductions/Subsidy Under Section 80C, Section 24, 80EE, 80EEA, CLSS.

- Personal Loans: Indirect Deductions as per Use of the Loan.

Is Heloc interest tax deductible IRS?

Interest paid on home equity loans and lines of credit is only deductible when you use the proceeds to buy, build or substantially improve your home that secures the loan.

How is equity taxed?

When you sell the shares, any gain is subject to the favorable long-term capital gains tax rate. The spread—the difference between the strike price and the market price on the date of exercise—is taxed as ordinary income in the year of exercise and is subject to income and payroll tax withholding.

How much tax do you pay on equity?

Generally, any profit you make on the sale of a stock is taxable at either 0%, 15% or 20% if you held the shares for more than a year or at your ordinary tax rate if you held the shares for less than a year. Also, any dividends you receive from a stock are usually taxable.

Is a home equity loan tax deductible in 2021?

Interest on a home equity line of credit (HELOC) or a home equity loan is tax deductible if you use the funds for renovations to your home—the phrase is “buy, build, or substantially improve.” To be deductible, the money must be spent on the property in which the equity is the source of the loan.

How does home loan affect taxes?

Homeowners may deduct both mortgage interest and property tax payments as well as certain other expenses from their federal income tax if they itemize their deductions. In a well-functioning income tax, all income would be taxable and all costs of earning that income would be deductible.